In February 2024, the Egyptian Government approved Law No. 7 of 2024, regarding the amendment of certain provisions of Article No. 8 and Article No. 13 of the Income Tax Law, promulgated by Law No. 91 of 2005 concerning the tax on salaries.

Who did the changes apply to?

These changes apply to employees and those involved in various sectors, such as commerce, real estate, intellectual activities, and non-commercial endeavors.

When did the changes take effect?

These amendments came into effect on 1 March 2024. For business activities, occupations, and real estate revenues, the new rule applies from the tax period ending after the publication of the act.

The purpose of these amendments

These amendments seek to establish an integral system to restructure income tax in Egypt with the aim of preserving social justice, supporting investments, enhancing digital transformation and the electronic tax system, and expanding the number of individuals benefiting from tax exemptions.

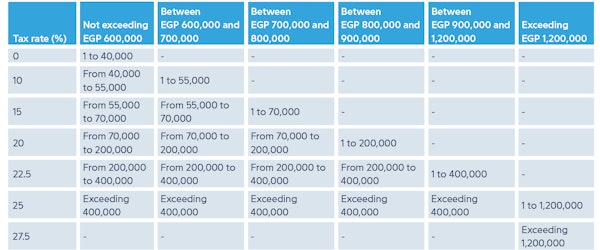

Key amendments introduced by Article No. 8

The new regulation has increased the lower tax brackets for the tax year 2024 as follows:

Taxpayers with a higher net taxable income are not allowed to take advantage of the lower tax brackets:

The annual net taxable income, ranging between EGP 600,000 and EGP 700,000, is not eligible for the 0% tax bracket.

The annual net taxable income, ranging between EGP 700,000 to EGP 800,000, is not eligible for the 0% and 10% tax brackets.

The annual net taxable income, ranging between EGP 800,000and EGP 900,000, is not eligible for the 0%, 10%, and 15% tax brackets.

The annual net taxable income, ranging between EGP 900,000 and EGP 1,200,000, is not eligible for the 0%, 10%, 15%, and 20% tax brackets.

The annual net taxable income, above EGP 1,200,000 , is not eligible for the 0%, 10%, 15%, 20%, and 22.50% tax brackets.

Article 13

The annual personal exemption for the individual and disabled individual taxpayer has increased as follows:

Note: The annual personal exemption limit has been changed from EGP 15,000 to EGP 20,000.

The annual personal exemption limit for a person with disability or caregiver for a person with a disability has been amended to 1.5 times the annual personal exemption. Hence, the limit of annual personal exemption in this case would be EGP 30,000.

How these amendments positively affect the individuals & the economy

For individuals, these amendments are aimed at relieving the tax burden on low- and middle-income earners. By adjusting tax brackets and rates, the revised income tax law ensures a fairer distribution of the tax burden. This provides relief to individuals, allowing them to retain a larger portion of their income. Increased disposable income will have a positive ripple effect on individuals’ quality of life, leading to improved consumer spending and a boost to the overall economy.

In addition to the direct benefits for individuals, the amendments to the income tax law also impact Egypt’s economy as a whole. By reducing the tax burden on individuals, the revised law stimulates consumer spending, which drives demand and supports businesses across various sectors. Increased consumer spending can lead to more job opportunities as businesses expand to meet rising demand, ultimately contributing to economic growth and reducing unemployment rates.

Conclusion

As Egypt continues on its path of development, Law No. 7 of 2024 serves as a testament to the Government’s commitment to creating a fair, transparent, and prosperous society. The implementation of this law is expected to have a profound and positive impact on the lives of Egyptians, as well as the overall economic landscape of the country.

ARTICLE BY

Amr Maher

AHG, Egypt

E: a.maher@a-h-g.net

Related news

-

18 September 2025

Member Spotlight - Morison LC, Malaysia

-

21 August 2025

Member Spotlight - HHP, Austria

-

19 June 2025

Member Spotlight - Alkhuzam & Co., Kuwait